Think back to this time last year. Consider how much has changed. Equity markets were ripping to new highs on the back of a stimulative tax cut, whispers of inflation were beginning to surface, and sentiment was reaching historically bullish levels. Now, just a short time later, the S&P 500 plunged over 9% in December to bring 2018 returns to negative – the worst year for the market since the Great Financial Crisis.

Investors are spooked that the Fed has overshot with its rate hike path. More drastic than the stock market, though, is the swift and dramatic change in the niche cryptocurrency market, plucked from relative obscurity to reach full-blown mania in 2017, soon followed by an incredible bust in 2018. The proliferation of cryptocurrency is thought to be a potentially disruptive force in several areas of commerce, but the volatility in the coins using this technology has led to massive sentiment-driven swings in value. After the two most popular cryptocurrencies (Bitcoin and Ethereum) each went up over 10-fold in 2017, both have collapsed during 2018 by over 75% so far, hampered by regulatory concerns and waning institutional interest.

If there is a definitional example of a mania in modern times, the cryptocurrency phenomenon of 2016-2018 rivals only the dot-com bust in the late 1990s-early 2000s (or Beanie Babies, but we’ll get to that later). All the classic signs of a bubble were present from an explosion in ICOs (initial coin offerings – the cryptocurrency market’s complement to a stock IPO) to an increase in fraud and institutional capitulation. Over $5 billion was raised in ICOs in all of 2017 and more than $6 billion was raised through ICOs in just the first quarter of 2018. A study by cryptocurrency advisory firm Statis identified over 80% of these offerings as scams. Several news stories identified companies that added “blockchain” to their names only to see their stock prices rocket higher, despite their unrelated principal businesses ranging from biotechnology to bottled iced tea, which is reminiscent of the “pets.com” madness of the dot-com era. Individual investors with no knowledge of the cryptocurrency market (other than its grand rise) nor the underlying technology found themselves investing their life savings in it.

In addition to the unfortunate individual interest, 2017 also saw institutional interest in the cyrptocurrency market gain steam as several Wall Street blue chips opened market-making operations. New crypto-related indices were created, Bitcoin futures were launched at the CME, and several institutional money managers identified cryptocurrency as a source of “uncorrelated alpha.” As we began to evaluate a few of the exchange-traded Bitcoin products, we learned that they traded at huge premiums to their underlying assets, reflecting insane levels of optimism by speculators. We also learned through industry scuttlebutt that many hedge funds had begun dabbling in trading the cryptocurrencies if not outright mining them, while others were allocating a decent portion of NAV to investing in this new asset class for the long term.

Now, over a year later, many of those institutional crypto desks have quietly shuttered. The volume and open interest of the Bitcoin futures market has failed to show traction, the kiss of death for any new product in financial markets. The previously excited hedge funds have stopped talking about it. This is understandable given that the HFR Cryptocurrency Index is down 66.82% YTD through November. The SEC has rejected several applications for new exchange-traded products based on crypto, a few of which had up to 300% leverage attached. Regulators are cracking down on bogus coin marketing schemes. And some of the most popular coins have plunged in value by more than 80%.

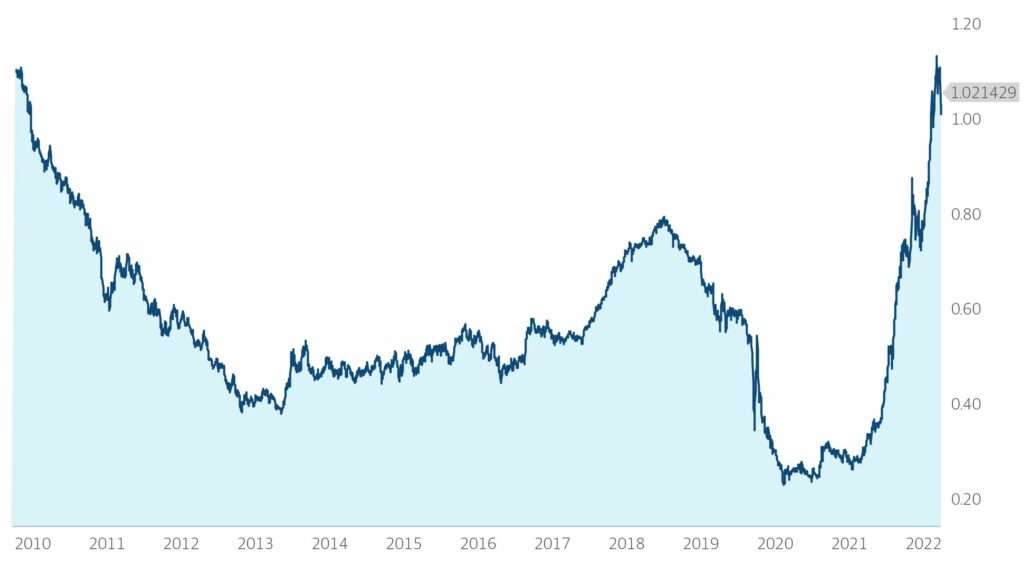

As the fall continues, with Bitcoin breaking below $4,000 USD/BTC after peaking near $20,000, the logical question is where the crypto market is heading. And it’s truly a question; the cryptocurrency market has shown strikingly similar behavior before. Bitcoin went all the way from $117 on May 1, 2013 to $1,151 on December 4, 2013 before making its way back down to $375 on December 6, 2014. The most recent time period occupying the same number of days exhibited very similar behavior: starting May 19, 2017 at a value of $1,988, it peaks on December 16th, 2017 at a closing price of $19,497 (it did briefly touch a bit higher the next day) and follows up with a decline to $4,079 on December 24, 2018.

Looking at the chart above, you can see that this recent bout of volatility is nothing new for Bitcoin and one should not lightly conclude that it has run its course on price action alone, which many are doing. In fact, one could argue that the 2013-2014 period was more volatile and exhibited more bubble-like features than the more recent period because the increase in price happened much quicker than the more recent one. The most recent loss in value is simply its most public one. But, please don’t take this to mean that we think these sudden run-ups in value will become a recurring theme. In financial markets, one rarely finds something that repeatedly and predictably happens. With Bitcoin, we believe that the last time was most likely the last time.

For one, you’ve got the public nature of its crash. My grandmother now knows what Bitcoin is. I mean, she doesn’t understand it, but she knows that it went through a little bit of a “rough patch.” My grandmother doesn’t like to invest in things she knows are volatile. Most others don’t either, and now you’ve got a “fooled me once” mentality among the masses where you did not before.

Second, financial regulators are now more aware than ever of Bitcoin and of the cryptocurrency market in general. They’re starting to crack down on those that advise on it without registering as an investment advisor and those that issue ICOs without going through the formal process of registering a public security. China outright banned Bitcoin trading while the US and EU are forcing Bitcoin custodians to follow Know Your Client and Anti-Money Laundering regulations that apply to all other custodians. The IRS and other tax-collecting entities across the world are beginning to use that data to find and fine those that don’t pay taxes on their cryptocurrency gains. Other three-letter agencies have employed sophisticated technology alongside the information the custodians have been required to provide in order to de-anonymize the owners of Bitcoins and those they transact with. Because of its use of blockchain technology, the government can see whom the owners paid and presume what they paid for from that information and other information they’ve gathered from other sources all over the internet. Wasn’t anonymity one of the major features of Bitcoin?

Third, there are many other options available. Bitcoin was just the first to catch on. For good or bad, there exist plenty of other cryptocurrencies with a variety of features for those that want to plant their stake in the ground on something other than Bitcoin with the belief that it will surpass Bitcoin. Yes, it’s true that it’s possible to create your own cryptocurrency using the same technology that Bitcoin uses. We could easily fork their code and start our own cryptocurrency called MangoCoin, named after Charlie’s dachshund. This would be similar in nature to DogeCoin, an actual coin launched years ago that was ironically named after the internet meme of a Shiba Inu. It currently has a market cap of $276 million U.S. Dollars. There are coins that are more appropriately named and not only match what Bitcoin is able to provide but have been programmed to have features that provide much more in terms of usefulness, like Ethereum or Ripple. Hundreds of coins exist and each has its own unique “selling point” to get users to buy in.

As we briefly touched on earlier, we spent some time last year evaluating the asset class and exchange-traded trust vehicles, which would have fit within our ETF mandate. It is a market that certainly exhibits signs of technical signals, which is a positive feature, but the giant premium to NAV embedded in the trusts presented an obvious problem for our approach.

The biggest issue for us, and one that we continue to grapple with, is how to appropriately “value” Bitcoin or any other major cryptocurrency. Before the crypto enthusiasts hit us with the “but how do you value any currency?” argument, let us be clear about one important factor; we aren’t necessarily confused about how to arrive at a target valuation for a particular coin (we are), but instead question why a given coin should have more or less value than another coin. We’ve seen plenty of arguments, but none especially compelling.

A recent piece on Investopedia entitled “Why do Bitcoins have value?” lays out several assumptions, the first of which reads: “Our first assumption is that Bitcoin will derive its value both from its use as a medium of exchange and as a store of value…if Bitcoin does not achieve success as a medium of exchange, it will have no practical utility and thus no intrinsic value and won't be appealing as a store of value.” Think about that for a second. Being a medium of exchange is what gives it its value. It’s a bit circular –for it to have value, one must be able to pay people with it, but for people to accept it as payment, it must first have value. And it isn’t important that there is actual inherent value, like there is with gold (industrial applications) or fiat currency (pay your taxes). The creators of each cryptocurrency are bootstrapping them by getting people to speculate on their future value via ICO.'

The tax-driven view of money states that what gives currencies around the world their value (or lack thereof) is each government’s ability to tax its people. Governments start their own currency because they themselves need the ability to transact – to direct economic activity. But there’s no single actor requiring payment in Bitcoin or any other digital currency. Bitcoin is not a tool to be used in the economy. Which means that the first large authority to do so with a digital currency just might dictate which digital currency wins the battle. Perhaps one that, instead of anonymity, strips that anonymity from everyone so the purchaser’s identity can be proven. That sounds like something a government would do. Until then, we may see Bitcoin hold onto top position or we may see a different, more agile and capable one, move to the front.

And Bitcoin is probably one of the worst for that government job. Since Satoshi Nakamoto limited the overall supply to a constant number of Bitcoins, 21 million of them to be exact, it would be hard for a government that adopted Bitcoin to expand the money supply to finance its debts or create economic prosperity – a useful feature of fiat currency. At a high level, inflation is a goal of the government – it sets a target inflation rate. Currently it is 2% per year. This allows the government to issue treasury debt that devalues over time. Thus, when the government sells $1 trillion in 10 year notes at 2.668% with a long-term 2% inflation rate, they end up repaying only $1.06 trillion in today’s dollars in total at the end of the ten years rather than the $1.26 trillion they otherwise would without inflation. Without the ability to inflate a cryptocurrency, where does this leave a government’s ability to borrow and repay?

Besides all that, there is governmental risk in owning and controlling a digital currency. Cryptocurrencies still rely on miners to confirm transactions. It would become a national security risk. If the United States went all crypto and did away with cash with a coin that somehow solved the above problem, a foreign power or powers could utilize the 51% attack and reverse transactions and double-spend coins or even worse, hold up all transactions, causing all sorts of chaos. If Russia and China joined up together, they’d put us down with ease. Can you imagine the propaganda? “Mine GovernmentCoin – For Your Country!” And since you must use your own electricity source for this, you’d literally be paying money to support the system of government payment. Maybe there should be tax credits for that.

These are just theories and in the world of free and open-source software where individual freedom, and anonymity are held in high regard combined with the fumbling bureaucracy that oftentimes is the federal government, we wouldn’t expect to see a government-sponsored digital coin show up anytime soon. And if we do see that at any time, we should certainly be asking who in the administration owns the first coins. Nor do we expect to see the kind of currency speculation we’re seeing today ending anytime soon – at least not until either a government does step in and say “we accept as payment for your taxes our fiat currency as well as this digital currency,” or people wise up to the fact that one coin is only good as long as there’s a large group that continues to believe it’s the best coin (which can change as quickly as new software code is written) and votes with their money.

Because of these views, we wouldn’t speculate here with our own money, much less client money. There will always be a core cabal of individuals or groups that hold any given cryptocurrency, which will inherently give it value, but why bother? If you put 5 coins in a digital wallet and forget about them, you won’t have anything other than those coins years later (if your hard drive doesn’t crash). Raw price appreciation. It’s anybody’s guess if the coin’s value kept up with inflation. If I put money in a stock, I’ll know that the company is at least generating revenue and (should I choose wisely) profits which I’ll have a claim on. Perhaps the company grows over time and the stock shows price appreciation as well. This is how value is created; not through popularizing an item so much that its own scarcity leads to an increase in value. Because at the end of the day, what’s the difference between a Bitcoin and a Beanie Baby?

After all, Beanie Babies had value too. Keep in mind this was in the late 90’s/early 2000s: Ty published a Collector’s Value Guide on a regular basis that contained reference market values for each Beanie Baby they had created. Kind of like Beckett for trading cards. It was a real market! One Amazon reviewer commented on a Collector’s Value Guide on July 4, 1999 that “I purchased this book to keep track of all of my investments, and it has done just that. It is a great book that gives you everything that a beanie babie (sic) collector needs to know. But on the downside, it has left out some of the prices for some strange reason. That's why it is only 4 *'s.” People saw Beanie Babies quite literally as investments. On at least one occasion, divorcees were ordered to split their “portfolios” of Beanie Babies under supervision in open court.

And here’s another Amazon review from May 31, 2002 for the Winter 2002 (published November 2001) Beanie Babies Collector’s Value Guide: “I was so upset when I recieved (sic) the book in the mail. Unless the book is wrong, beanie babies are going out of style. The bears (sic) prices have dropped anywhere between 10$ and 60$. It (sic) starting to scare me, I'm wondering if I made a bad investment!?” If you asked one of those individuals that invested their life’s savings in Bitcoin, they’d certainly say that history does repeat itself after all, complete with “theft, fraud, and fakery.” These days, Charlie’s wife uses Beanie Babies at school for bean bag tosses with the children. At least there’s some residual value. What can you do with a digital coin gone defunct?

That’s not to say that the technology currently has no value at all and is completely speculative. In fact, our view is that the blockchain technology that underpins cryptocurrency has disruptive potential in many areas including healthcare, real estate, and finance. The decentralized system that is the main feature of blockchain allows the system to record transactions in a secure, open ledger and in many cases cuts out unnecessary time and middlemen. Ripple (XRP) is already being used as a processing mechanism for international bank remittances. We’ve seen compelling cases for a blockchain-based system to ultimately replace stock exchanges, real estate titles, and health care records.

Ultimately, we think that the best opportunities to make money in the space are probably not in speculating on the value of the coins themselves, but instead through equity investments in transformational growth companies with a strong business case using blockchain technology. We of course aren’t recommending any specific investment and acknowledge the vehicles to access these investments may be out of reach for many investors. In most cases, these companies are private, which means that a specialty private equity fund is probably the most accessible vehicle for most investors. There is much risk here, so we would implore any interested investor to do his or her own homework and seek appropriate counsel. Still, with blockchain-based business still in the early innings, we believe the sector deserves a thorough look.

Thank you to everyone for your feedback. Please feel free to reach out at any time with questions or comments.

Sincerely,

Arthur Grizzle & Charles Culver

Managing Partners

Martello Investments